Live Like Royalty with Mezzanine-Financed Community Investments

Natural royalties overcome pitfalls of heavy debt loads and uncertain equity payouts.

Most companies, young and old, use a combination of loans, bonds, stock, and partner shares to fund projects and growth. It seems simple enough and works alright from a broad perspective.

Zoom in a bit more to the small business landscape and things aren’t alright. Both of the fundamental financial instruments, standard debt and equity, come with pitfalls that make it difficult for lenders and borrowers to work out a stress-less mutually beneficial arrangement over the long term. There’s a reason that wise sages have warned us about the dangers of usury and predatory loans for millennia. Usury eventually leads to extreme income and wealth inequality, which has become clear in recent years.

Better investment returns with lower risk are achievable. Adoption of natural royalties might even lead to collective control of the economy by the community rather than radical power consolidation by multinational banking conglomerates.

Kevin O’Leary from CNBC’s Shark Tank TV show popularized a basic form of the decentralized alternative. Royalties differ in their exact mechanics, but they all share the trait that payments are made as a percentage of sales or gross income, similar to taxes and tithes. As revenue goes up, the company can afford to pay off its investors.

With equity, much of the decision about when to pay back investors is made by whoever controls the board of directors. An executive team could delay dividends and buybacks indefinitely, giving financiers a long and uncertain investment horizon. If the company never turns a profit, equity investors might not see a dime of their money back. Debtholders get first dibs on salvaged assets and bank accounts after bankruptcy. If investors foresee that in advance, they could take control of the board and drain the company of its resources before it has a chance to really take off into profitable territory.

Silicon Valley invests billions of dollars into young ventures every year. That sounds like more than enough money to go around, but over 75% of early-stage venture-backed startups fail within a few years, which might have something to do with the outdated financial instruments used to fund them. Founders and angel investors frequently get smaller payouts than expected, or they inadvertently spend away their venture capital investments without the proper managerial disciplinary incentives in place.

With conventional debt, the calculation of how much a company owes is fairly simple, but paying it back is another story. A founding team can lose control of the company incredibly quickly after missing a few months of loan payments. Even if profitability goes way up a few years later, it might already be too late for the founders to regain ownership and catch up with the exponentially-rising debt burden. If a founding team loses ownership, they also tend to lose motivation, and nobody is left to carry the company into its golden years of profits. In many cases, it’s a lose-lose situation for debtors and creditors. Neither partner gets a great low-risk return on their investment.

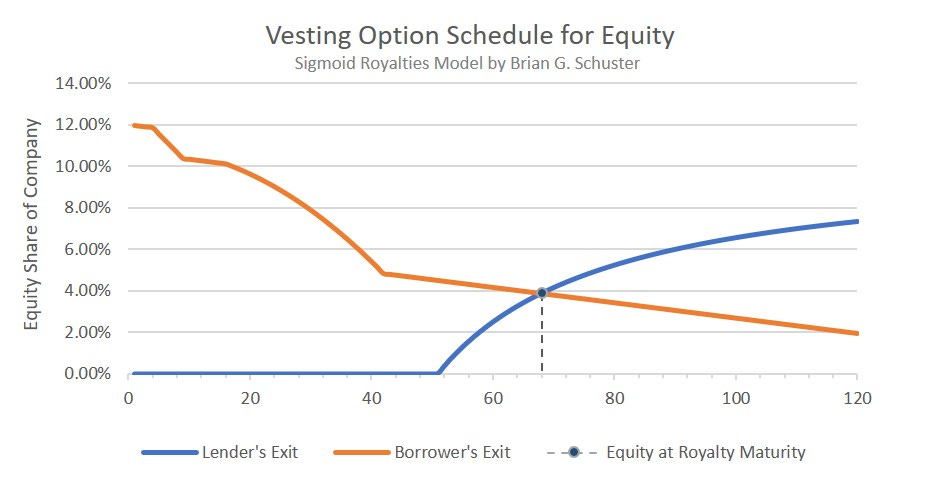

Natural sigmoid royalties have the characteristic of debt in the sense that there is a certain expectation of when the royalties should be paid back, but they offer flexibility about how a company deploys its capital during its sensitive early stages of growth. They have the characteristic of equity in the sense that both parties agree to a valuation upfront, and that valuation determines what fraction of a company’s equity shares the investor gets if the borrower fails to pay them within the allotted time period. The equity shares earned depend on which party—investor or business owner—decides to proceed with the vesting option.

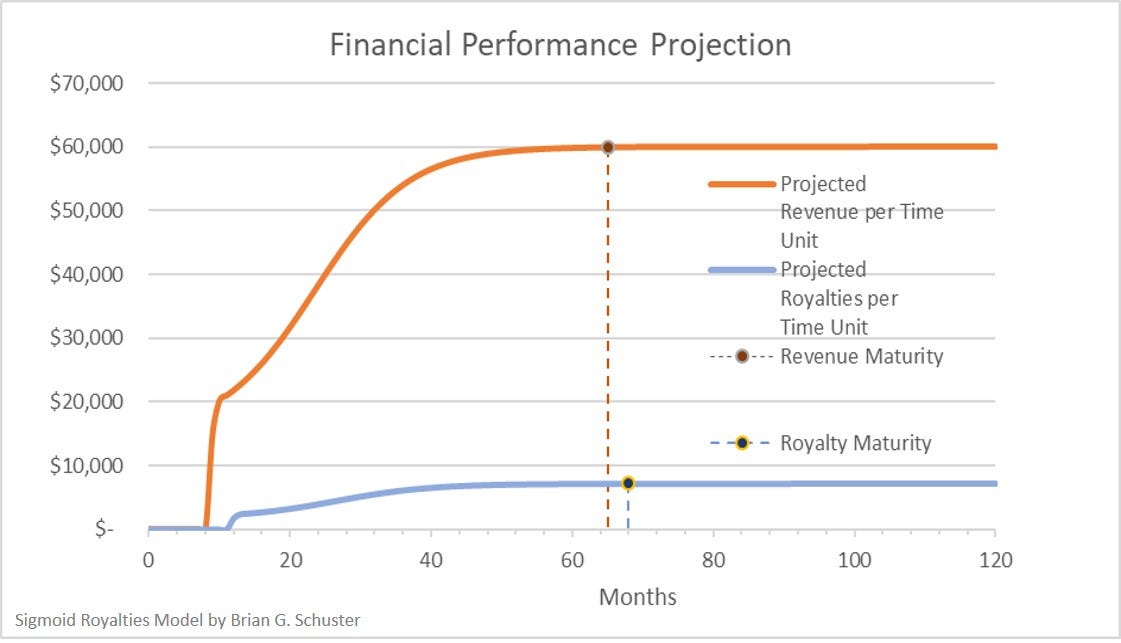

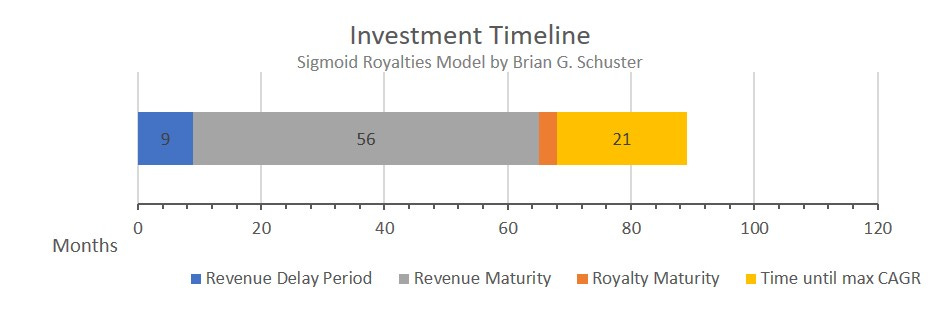

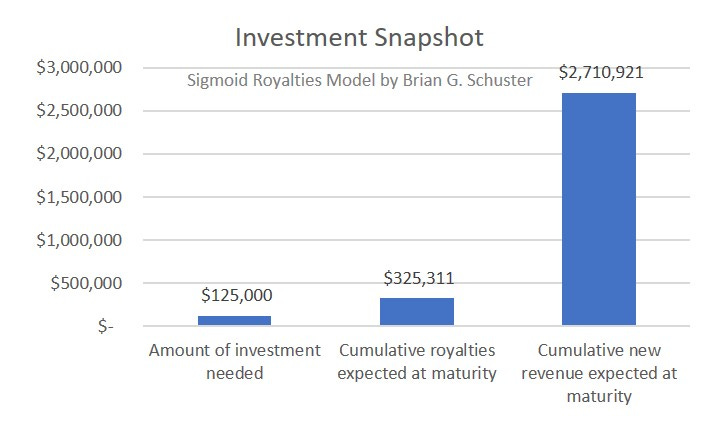

Graphs are shown below to illustrate the natural sigmoid royalty concept on a monthly basis. If you’re not familiar with financial models, balance sheets, and income statements, it’s best to learn about those first before jumping into mezzanine royalties.

The sigmoid descriptor describes the S-shape of the logistic curve that mimics naturally bounded revenue growth during the investment horizon. The curve differs starkly from boundless exponential growth that never tapers off until a conventional loan is paid off.

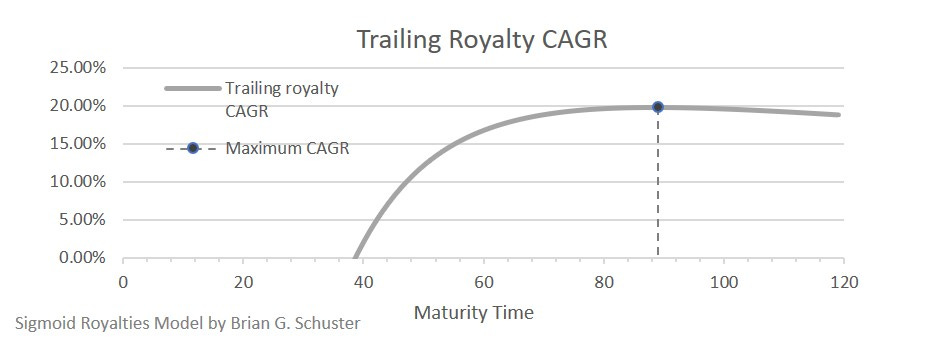

CAGR indicates annual returns. Equity vesting indicates how much of a company the investor gets if their firm or the borrower decides the company can’t pay the full amount of royalties.

The concept has applicability to venture investments, but it can also be used to invest intellectual capital or labor into a young business that doesn’t have tons of cash yet wants to attract top-tier talent. Skilled consultants, employees, salespeople on commission, and contractual hires could earn good money as the company grows. It’s a recipe to achieve tax-advantaged alignment of incentives with realistic growth targets.

Let me know if you’d like to try out a different scenario in the financial model! Parameters are adjustable as shown in the appendix.

Appendix

Standard terms used as variable model inputs: existing revenue; revenue growth targets; revenue delay period; revenue maturity period; payment grace period.

Optional terms:

Retainer or signing bonus for intellectual capital (intC) investments

Base minimum payments with delay for intC

Capital asset sale restrictions for monetary capital (monC) investments

Slow release of investment by escrow according to revenue milestones for monC

Option to transact royalty contracts as royalty bonds

Restrictions against conventional debt (protection from usury)

Do you have an accountant friend who could benefit from this? Photo by Nomadic Julien on Unsplash. This article may be shared under Creative Commons license CC BY-ND 4.0.